“One today is worth two tomorrows” (Benjamin Franklin)

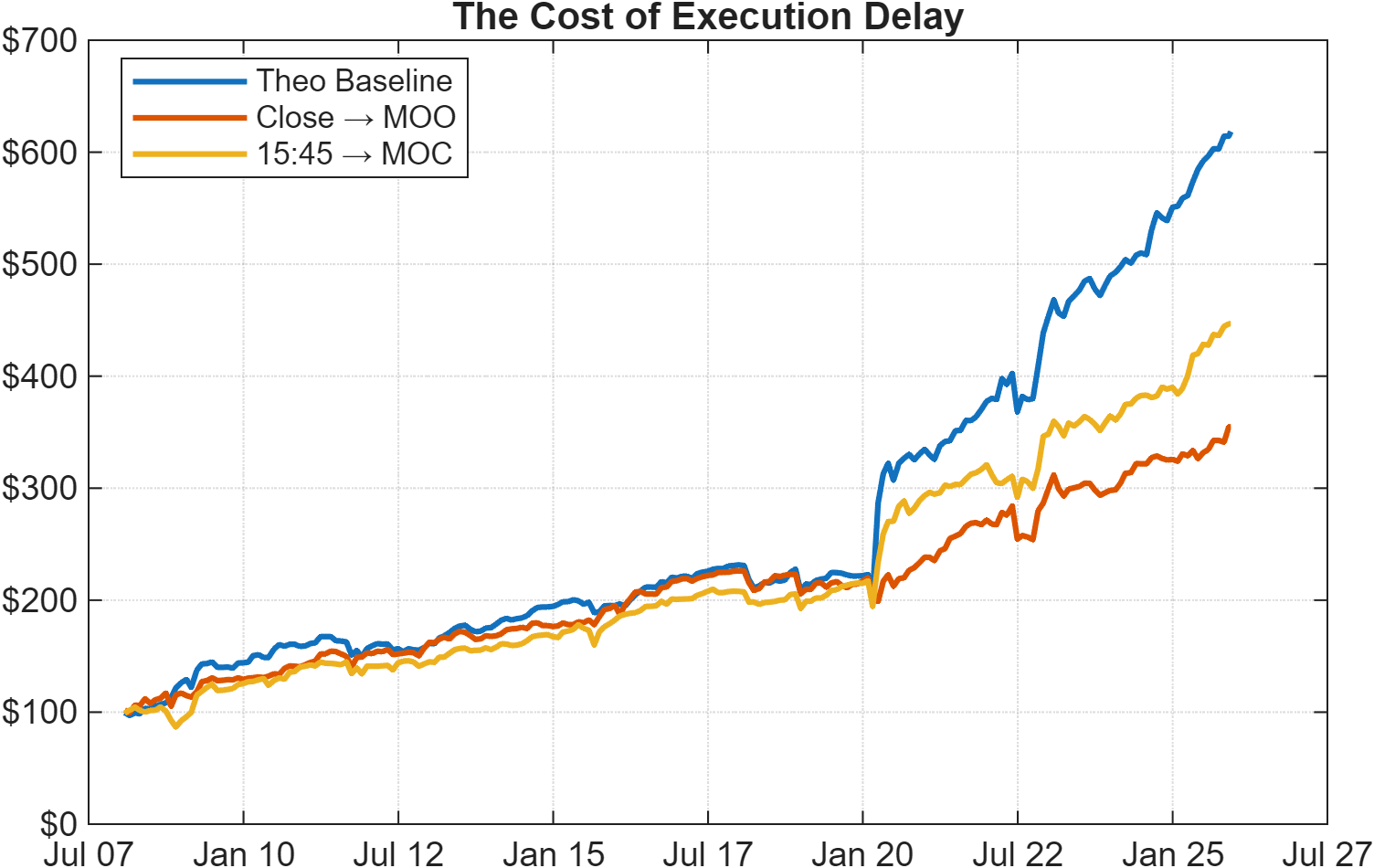

For many quantitative traders, a standard operational workflow can sound something like: compute a signal at the end of the trading session, execute at the next open, and keep live trading neatly aligned with an end-of-day backtest.

It is simple in practice and easy to explain, but our experience suggests it is often suboptimal.

If a signal decays slowly, executing it at the next day’s open should have limited impact. However, when the alpha is driven by short-term mean reversion or microstructure effects, the roughly seventeen-hour gap between 4:00 PM and 9:30 AM can erode a substantial portion of its predictive power.

Using intraday-resolution data, we compare two implementations: one that generates the signal at the close and executes at the next day’s open, and another that forms the signal 15 minutes before the close and executes via a market-on-close order on the same day. This allows us to address a question that research notes often avoid.

At what point does execution timing stop being an implementation detail and start becoming a first-order driver of performance?

Something worth noting is that execution policies are not just about speed.

Modern technology makes near-instant signal computation feasible, but certain windows of the trading session face particular liquidity challenges, with spreads widening and slippage risk increasing meaningfully.

We find that the balance between signal decay, signal-to-execution lag, and liquidity (particularly for short-term trading programs) is not a secondary concern: it can determine whether a compelling research result survives first contact with live execution.

If you found this article useful, feel free to leave a comment and reach out via direct message or email at info@concretumgroup.com for any questions.