“The world is changing very fast. Big will not beat small anymore. It will be the fast beating the slow” (Rupert Murdoch)

Most people assume institutions have an unbeatable advantage in trading. More capital, better technology, lower commissions, better access: end of story.

But there is one problem with that narrative: size is not always an advantage.

In many strategies, especially those that rebalance frequently or operate in less liquid names, the real question is not who pays the lower fee schedule, it is who can trade without moving the market against themselves.

A small order slips through seamlessly, whereas a large one can become its own source of friction.

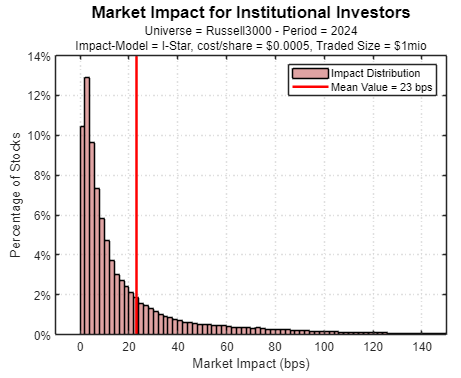

When looking at trading through the lens of market impact, we investigate a simple yet important question: when two investors run the same idea, how much of the difference in performance comes from their order size?

The answer matters more than ever as the old retail disadvantages are shrinking. APIs, automation and faster platforms have changed what an individual trader can realistically do from a home office.

Could it be that in certain areas of the market, retail investors may actually be structurally better positioned than larger players?

In our opinion, this matter deserved a proper quantitative evaluation, and if you’re not yet familiar with the models that researchers can use to estimate market impact…

…you can read the full article by clicking on the button above.

If you found this article useful, feel free to leave a comment and reach out via direct message or email at info@concretumgroup.com for any questions.