Introduction: The Legacy of Value Investing

Value investing has been one of the most enduring investment philosophies, pioneered by Benjamin Graham and later popularized by Warren Buffett.

At its core, value investing is based on the idea that markets are not always efficient, and mispricings occur, allowing investors to buy stocks at a discount to their intrinsic value.

Graham, in Security Analysis (1934) and The Intelligent Investor (1949), emphasized the importance of buying stocks with a margin of safety, meaning stocks that trade below their fundamental value as measured by earnings, book value, or cash flows.

Buffett, Graham’s most famous student, refined this approach by incorporating qualitative factors such as economic moats and strong management teams.

The Academic Perspective: Quantifying Value Investing

Academia has long sought to quantify the stock selection process used by successful value investors. A key breakthrough came with Eugene Fama and Kenneth French (1992, 1993), who introduced the High Minus Low (HML) factor in their three-factor model. Their research showed that stocks with high Book-to-Market (B/M) ratios (a proxy for cheap valuations) tended to outperform stocks with low B/M ratios over long periods.

Subsequent studies expanded on this by testing different valuation metrics such as price-to-earnings (P/E), price-to-cash flow (P/CF), and enterprise value-to-EBITDA (EV/EBITDA).

Across different markets and time periods, the evidence consistently supported the existence of the value premium, whereby cheap stocks tended to generate higher risk-adjusted returns than expensive stocks.

Empirical Evidence: Performance of Value Portfolios

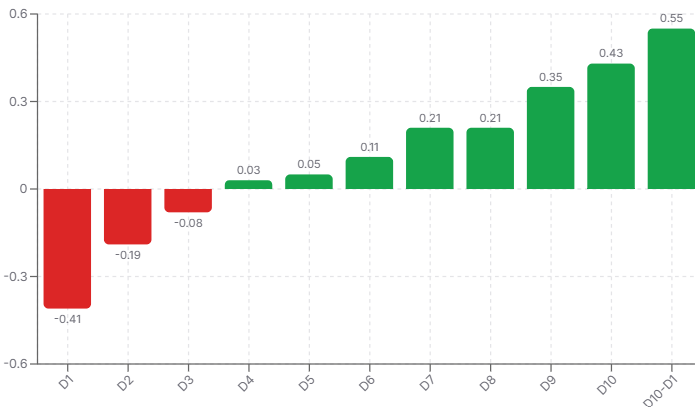

To visualize the strength of the value premium, the following chart presents the alpha of decile portfolios relative to the CAPM model, sorted by Book-to-Market ratio, from 1926 to 2026. The decile with “cheap” value stocks is D10.

The chart reveals a nearly linear relationship between monthly alphas and value deciles, demonstrating that stocks in the highest B/M decile (Decile 10, the most undervalued) generated the highest excess returns, while those in the lowest B/M decile (Decile 1, the most expensive) performed the worst.

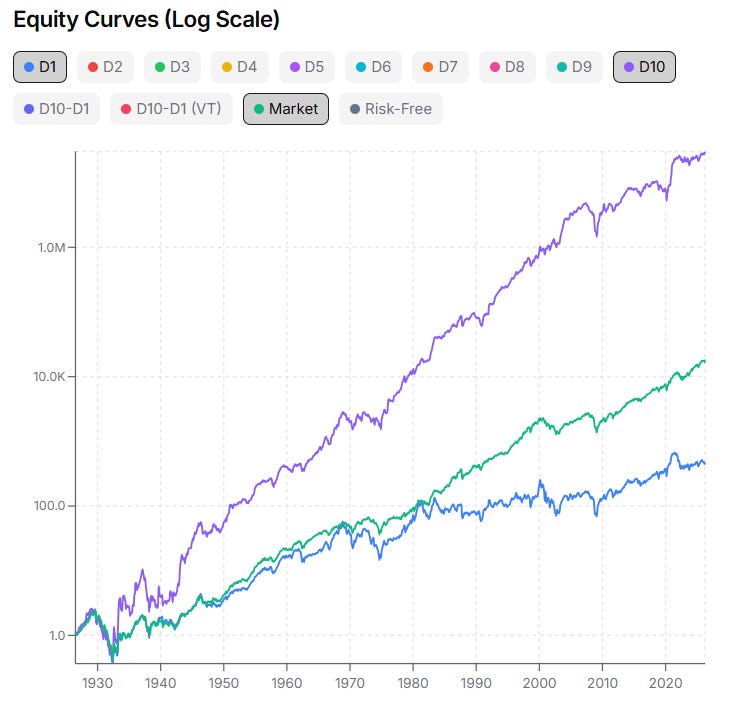

This pattern is also evident in the equity curve below, where Decile 10 (high-value stocks) consistently outperforms Decile 1 (low-value stocks), reinforcing the historical advantage of investing in undervalued companies.

Why Does the Value Premium Exist? Risk vs. Behavioral Explanations

The persistence of the value premium has sparked debate on whether it is a compensation for risk or a market inefficiency due to behavioral biases.

Risk-Based Explanation

One view is that value stocks are fundamentally riskier investments, and their higher returns compensate for this additional risk. Value stocks often belong to companies that are financially distressed, operate in declining industries, or have uncertain growth prospects. During economic downturns, these stocks tend to suffer more than their growth counterparts. Fama and French (1993) originally supported this explanation, arguing that value stocks load on risk factors not captured by traditional CAPM.

Another argument for the risk-based explanation is that value stocks are more sensitive to macroeconomic conditions, such as changes in interest rates, inflation, and credit cycles. Investors may demand a premium for holding stocks that are more exposed to these risks.

Behavioral Explanation

However, alternative behavioral theories emerged, particularly in Lakonishok, Shleifer, and Vishny (1994), which argued that the value premium arises from investor overreaction and mispricing rather than risk. Investors tend to suffer from representativeness bias, a situation where they naively extrapolate past earnings growth rates too far into the future.

The chart below, taken from the great book Quantitative Value by Wesley Gray, Ph.D. and Jack Vogel, shows the average past five-year earnings growth rates for each decile portfolio formed on the Book-to-Market metric.

It is evident that the more a stock is classified as “Value” (i.e., higher book-to-market ratio), the lower its recent earnings growth. The relationship is almost perfectly linear.

Now the question is:

Do value stocks with low earnings growth rates continue to exhibit low earnings growth in the future?

The answer is provided in the figure below and is a decisive NO!

Value stocks in the top decile tend to have the highest future earnings growth rates, making investors not only buy at a low price relative to book value but also buy stocks that, on average, tend to have higher earnings growth in the future. In some sense, this chart suggests that value investing exposes investors to stocks that will become some of the fastest-growing stocks in the future.

Challenges of Value Investing and the Role of Momentum

One challenge of value investing is that it can experience prolonged periods of under-performance relative to the market. Investors with short-term investment horizons may find it difficult to stick with value strategies, as these drawdowns can last for years. A notable example occurred in the late ‘90s when value stocks dramatically underperformed the broader market. During this period, often referred to as the dot-com bubble, even some of the most successful value investors suffered significantly. For instance, Julian Robertson’s Tiger Funds saw its AUM decline sharply, while Barron’s magazine questioned whether Warren Buffett had lost his magic touch.

This has led to the search for ways to enhance value investing, and one of the most effective methods identified by both academics and practitioners is combining it with momentum investing.

Well-known academics and practitioners, such as Cliff Asness, Tobias Moskowitz and Lasse Pedersen, have shown that adding a momentum leg to a value strategy significantly improves risk-adjusted returns. The benefit of this combination is pervasive, not only in equities but also across other asset classes, including bonds, commodities, and foreign exchange.

In our own trading, for example, we also exploit the orthogonality between value and momentum signals when trading volatility. This diversification effect helps smooth out drawdowns and provides more consistent returns across different market environments.

Conclusion

Despite its historical success, value investing has faced challenges in recent years, particularly post-2008, when growth stocks dominated. Some argue that changing market structures and the rise of intangible assets have diminished the effectiveness of traditional value metrics. Nevertheless, value investing remains a fundamental strategy for investors seeking long-term outperformance, supported by both empirical data and the principles laid out by Graham and Buffett.

Interestingly, in 2020 and 2021, value stocks experienced a strong resurgence, with the top decile of value stocks returning 53% in 2020 and an impressive 91% in 2021 when constructed using an equally weighted methodology. This remarkable rebound highlights the cyclical nature of the value premium and underscores the importance of maintaining a long-term perspective when investing in value strategies.

While the debate over whether the value premium is a compensation for risk or an anomaly driven by behavioral biases continues, its long-term persistence suggests that patient investors can still benefit from applying value principles in a disciplined manner, potentially enhanced by the inclusion of momentum investing.

📊📈📉 The first 2 charts used in this article were generated using a FREE tool developed by the Concretum|Research team.

If you found this article useful, feel free to leave a comment and reach out via direct message or email at info@concretumgroup.com for any questions.

Disclaimer

This publication is provided by Concretum Group for informational, educational, and research purposes only. It does not constitute investment, financial, legal, or tax advice, nor a recommendation to buy or sell any security, instrument, strategy, or investment product. All investments involve risk, including possible loss of principal. Past performance, backtested performance, and historical analysis are not reliable indicators of future results. Readers should conduct their own research and consult qualified professionals before making investment decisions.

Full disclaimer: https://concretumgroup.com/disclaimer/