Most investors tend to have a directional instinct: they form a view on where prices are going and act accordingly.

Volatility traders, instead, ask a different question.

They do not care much whether the market rises or falls: they care whether it moves more or less than what options currently price in. That distinction may sound subtle, but it implies a fundamentally different source of return, one that, in principle, should behave independently of the equity market.

In this new paper, we analyze volatility trading with a particular focus on VIX ETNs, exchange-traded products that have grown increasingly popular in recent years, allowing traders to gain long and short exposure to the entire VIX futures complex.

The framework we lay down progresses through four rule sets, each adding a layer of predictive content to the signal used.

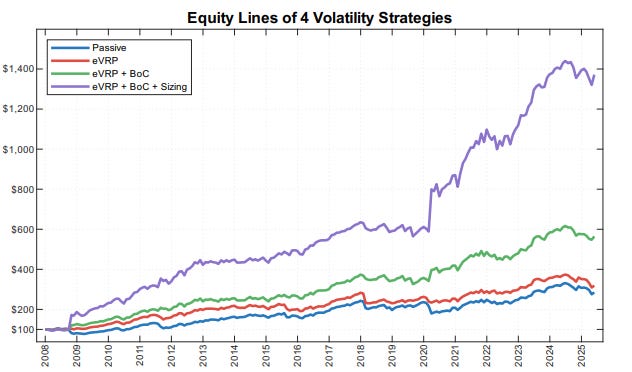

A purely passive short-volatility allocation serves as our baseline, delivering single digit returns, high drawdowns, and a 72% correlation to the S&P 500. Its purpose is simply to capture the volatility risk premium in its most basic form.

We then progressively enhance the framework through three key improvements:

Volatility risk premium filter: a signal based on the expected difference between implied and realized volatility

VIX term structure signal: a more forward-looking indicator that captures information embedded in the futures curve

Dynamic position sizing: a final refinement that adjusts exposure based on the current level of the VIX

Together, these enhancements transform the baseline strategy into a materially stronger framework: the Sharpe ratio increases from 0.48 to 1.00, CAGR rises from 6.2% to 16.3%, and correlation to the S&P 500 drops from 71.6% to just 14.8%, turning a fragile, equity-like exposure into a more robust and genuinely diversifying return stream.

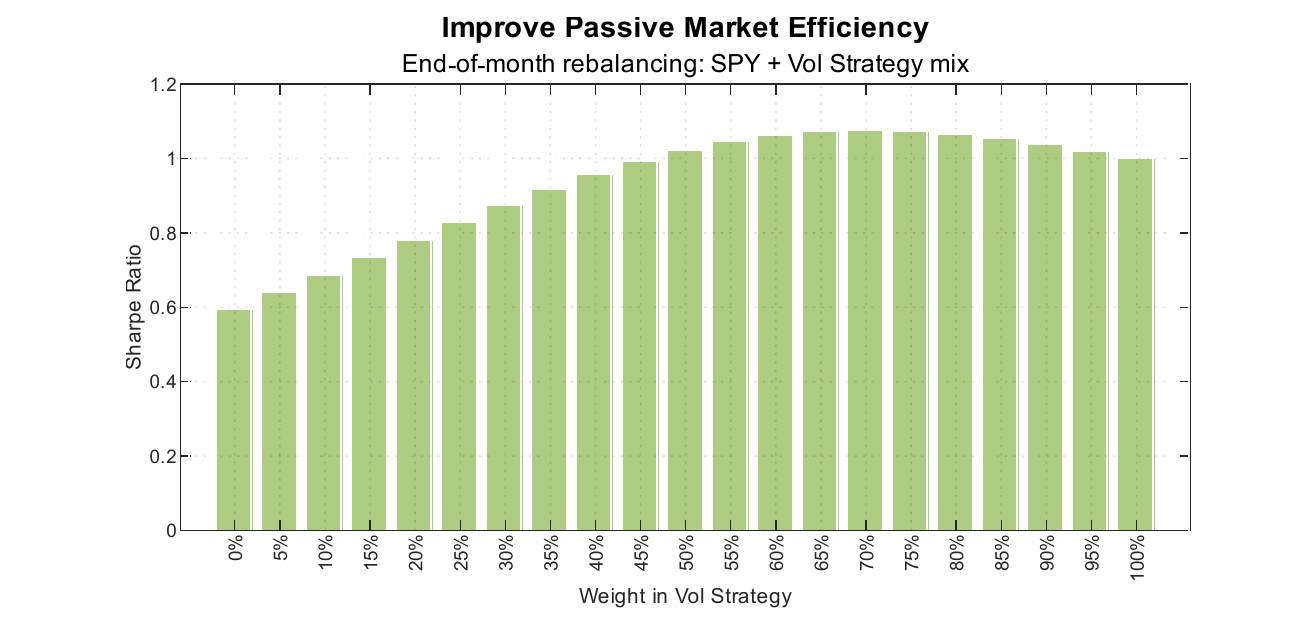

Beyond the strategy itself, we examine how a volatility sleeve of this kind interacts with a passive exposure on S&P500 (SPY ETF), finding consistently attractive results across a range of allocation specifications.

That said, we would like to close with a note of genuine caution: the volatility risk premium has been persistent, but (like anything in markets) it is not guaranteed, and any type of strategy in the volatility space demands constant sizing discipline and an honest accounting of tail risk.

As a practical extension, we also include Python code showing how this strategy can be implemented and automated through Interactive Brokers, bridging the gap between research and execution.

For the full methodology, details, and Python implementation code, we encourage you to read the paper.

If you found this article useful, feel free to leave a comment. You can also reach out via direct message or email at info@concretumgroup.com for any questions.